Someone to Answer For It

Money is one of very few things you exchange without asking questions about what it means, what it represents. A note crosses a counter, a balance moves on a screen, and the person taking it does not stop to ask who issued it, what stands behind it, or whether the party paying can be trusted to be good for it. You do the same a dozen times a day without a thought. The Bank for International Settlements, in the chapter it published on the twenty-third of June, gives that thoughtlessness its proper name and shows that it is not thoughtlessness at all but the deepest thing money does: money is accepted as final settlement with no questions asked, and that acceptance rests on a single property, the singleness of money, the guarantee that one unit is worth exactly one of every other unit of the same money, redeemable in central bank money, with finality. The questions go unasked because, somewhere behind the note, there is always someone to answer for it. Take that away and the questions do not vanish. They arrive all at once, and they arrive in a queue at the door of a bank.

That is the question underneath the whole noisy argument about stablecoins, and underneath the scramble of governments now trying to regulate them, though it is rarely put this plainly. Has any of it restored the chain of accountability that makes money work, or has it only moved the gap somewhere harder to see? The honest answer is the second, and the institutions best placed to know have now said as much in their own words. This essay sets out what digital money is for, why the versions on offer fail, how the regulators and central banks have diagnosed that failure correctly and not yet solved it, and what we have built to finish the work: the same instrument, rebuilt by the right hands with its safeguards restored, completing rather than replacing the regulated system, with neutral ground beneath it that no one owns.

What digital money is for

You already use digital money. Your salary lands in your account as a number. You tap a card and the number on screen confirms; you send a friend twenty Francs, Dollars or Euro - whatever currency you use - through an app and a number moves from your screen to theirs. None of it is cash, all of it is digital, and it works, right? So when a new industry arrives promising to invent digital money, the first honest question is the obvious one: to do what, exactly, that the number on your banking app does not already do?

The promise has a name, and for two years it has been the loudest pitch in finance. It is the stablecoin, and the case for it is genuinely attractive, which is why it is worth stating at full strength before taking it apart. A stablecoin is a digital token on a public blockchain, meant to be worth one dollar, always. Hold it and you hold a dollar that needs no American bank account, that moves to anyone on earth in seconds rather than days, that does not close at five o'clock or stop at a border. The pitch claims to deliver for the people the banking system serves worst: the worker abroad wiring wages home and watching fees and middlemen take their cut; the saver in a country whose own currency is melting, who wants dollars and cannot easily get them; the small exporter waiting three days and four banks for a payment to clear. Those are real problems. A dollar that travelled at the speed of a message would be a real answer to them. That is why the pitch works, it's the narrative that puts a moral veneer on the rather dirtier truth, which I will come to.

Here is the distinction the whole debate skips, and without it you cannot see what a stablecoin actually is. Two different things get called digital money, and they are not the same animal. The first is digitisation: taking something that already exists and putting it on a screen. A paper ledger becomes a database. A cheque becomes an electronic instruction. The pounds, dollars, yen, francs, Euro in your bank account are digitised in exactly this way. They are a number standing for a claim, and when you pay someone, no money travels; a message travels, and two banks update their records of who owes what, between themselves, later. The second is digitalisation: rebuilding the thing itself so that the value is the digital object, and settling a payment means the object itself has moved, finally, then and there, with nothing left for anyone to reconcile afterwards.

The first is a record of money that lives somewhere else, money you have permission to use, that you trust you will keep access to, and that you only ever control at someone else's sufferance. The second is money - cash. That second thing is not a fantasy and it is not new; it has been built once already, as a proof of concept, under a name everyone knows. Bitcoin's white paper is titled "A Peer-to-Peer Electronic Cash System," and that is exactly what it set out to be: value living as a digital object that settles itself, a claim on no one, issued by no one. It proved the thing could exist. What it could not do was hold its value or clear fast and cheaply enough to be money you would actually spend, and so the proof of the idea stood while the usable money never arrived. It was then transformed into something it was never intended by its creator to be: an amorphous 'store of value' to fit whatever argument (however inconsistent or logically flawed) was being made for the fiat price to go up.

That difference between the two different things that are called digital money is the whole game, and two failures have left its second half unbuilt. Bitcoin tried to build it and could not; the mainstream economy never tried at all. It digitised the old claims decades ago and stopped. Beneath the slick apps, settlement still runs on rails built for paper: payments gathered into batches and processed later, value landing days after the deal is struck, and across borders a relay of correspondent banks that is slow, costly and opaque, where a payment loses a day to a time zone and you cannot see where it has reached. Finishing the work, so that money moves and settles natively, in seconds, as an object rather than as a promise to square up later, is a real and large piece of unfinished economic business. The need is genuine, but the solution that has been provided to date is not the answer it masquerades to be for legitimacy it does not deserve.

Today's prominent stablecoins digitise your fiat money on someone else's ledger and dress it as the second - actual cash. It is not digitalised money but a digitised claim on a private reserve, wrapped on a public chain so that it wears the look of the thing it stands in for. Being a claim on dollars, it cannot escape what every claim on dollars carries: you may use it only by leave, you may reach it only for as long as you are allowed, and you never finally own it, only ever hold a promise that someone else honours. That much it shares with the dollars, Euro, francs, pounds and yen in your bank, and that much is fiat's nature rather than anyone's crime. The whole of the difference is what assurances the audited, regulated, responsible bank wraps around that dependence and the present stablecoin offering throws away.

The money in your bank account sits behind a wall built over a century: a reserve that is audited, capital the bank must hold against what it owes you, a supervisor who can fine it or shut it, insurance that pays you back when it fails, and a court that will hear you when it does not. You trust a middleman there too, but you trust one that others are paid and empowered to watch. The stablecoin keeps the dependence and pulls the wall down. You still cannot move the money without the issuer's leave, still rely on access you do not command, still hold it only for as long as you are permitted, but now there is no audited reserve you can count on, no capital standing behind the promise, no supervisor who can act, no insurance when it breaks, and no one under any duty to answer you. Measured against either thing it might have been, it falls short of both: it has given up the freedom of real digital cash, which needs no one's leave because it answers to no one, and it has thrown away the protection of bank money, which at least pays for the watching. What is left is fiat's full dependence stripped of fiat's only safeguards, a private IOU that settles nothing with finality and lets the issuer keep the float - and the interest, their true objective - on the money behind it. Which leaves a plain question standing in the open: who would take the naked claim over the protected one, and why?

The answer is not in the payments world the pitch points to. It is inside crypto, in a gap that Bitcoin's failure had opened there and left wide open. Picture crypto for what it is, a casino, and its tokens for what they are, the chips. Inside the house the chips move well enough: sell a freshly pumped token for Ether and that leg settles on the chain quickly enough to call it done - settlement. What it does not do is make the winner safe, because the chip he now holds is itself a thing whose price against the dollar will not sit still, and the Ether ledger gives him no final settlement in any case, only an entry that grows harder to reverse as blocks pile on top of it. He has swapped one floating thing for another. What he needs is not a faster way out. It is a stable denominator: a way to stop the number moving, to stand in the dollar, on the chain, and call the win real - or at least, closer to the true objective: a United States dollar in a United States bank account, fully, assured and secured.

There is no native digital cash on the chain to do that with, and the reason returns us to Bitcoin. Bitcoin failed at the one thing it was built to be, which was money you spend: it will not hold its value, and it cannot clear cheaply and quickly enough to be cash. That precise failure is why the casino cannot cash out into Bitcoin either. Bitcoin is the original chip, though it holds that place by betrayal rather than by design: it could not evolve into the money its own white paper promised, and it was then repurposed by people who found a price that only rose more useful than money anyone would actually spend. The proof of that failure is the whole stablecoin industry. If Bitcoin were spendable money that held its value, the winner would settle into Bitcoin and the dollar token would have no reason to exist. The dollar tokens that now exist, and the scale they have reached, are the market's own standing admission, written in its own money, that the thing built to be digital cash cannot do the job.

So the window was built the other way about. A dollar token living on the same chains as the chips lets the winner settle the exit on the chain itself, Ether to Tether, with no bank in the loop at the moment of cashing out, and Tether stepped into the breach Bitcoin had left. This is what the dollar token is for. It is not a payment rail; it is the cash-out rail of the casino, the device that lets a win be booked in dollars without leaving the chain. Here is why its missing safeguards are not merely tolerated by the people who matter most to it but wanted: an audited, supervised, fully compliant issuer would put back exactly the friction the exit exists to remove, the questions about where the money came from, the freeze that follows a regulator's nod, the refusal to serve a wallet with a history. The opacity is not a defect the insiders endure, it is the product they are buying.

Even then the dollar token is only a waypoint, not the destination, and seeing why is the whole of the matter. There are three states here, and only the last is final. The Ether is not stable and not final. The dollar token is stable in price but still not final, because its stability is a leap of unaccountable trust, convenient and expensive, holding only for as long as no one tests whether the dollars behind it are really there. Finality is the third state alone: ordinary dollars in an ordinary bank account, every assurance restored and, for the winner, the awkward questions conveniently unasked. The settlement that actually ends the exposure is not Ether to the dollar token. It is the dollar token to banked dollars, and that crossing is charged at both ends. While the money sits in the token, the issuer keeps the interest on the reserve and the holder earns nothing. At the gate, the on-ramps and off-ramps take their cut, and for the small holder the toll is set so high that he or she is all but invited to forfeit rather than pay it. The instrument sold as the dollar is in truth a tollbooth in front of the dollar, charging rent to wait in it and a fee to leave it. The thing that promises the winner his finality holds none of its own.

This is also why, for all the talk of institutional adoption, no one is building a stablecoin well, and cannot while this is what the instrument is for. Put the institutional case to the one question that settles it: who wants a representation of fiat that keeps every permission and discards every assurance, when they already hold the banked fiat it represents? No one who has the bank already. Take the casino out of the picture and the genuine paying demand for an unaccountable dollar token shrinks to something small and particular, the cash-out for crypto's winners and the use of those the regulated system will not allow near money at all. The crowd that fills the casino is held there by the displayed winnings of a lucky few, who exist, as in every casino, mainly to draw the rest in to be parted from their money; the house, the issuers and the insiders and their backers, takes its own winnings out reliably, and the unaccountable rail is what makes that extraction bankable. That is the shape behind the numbers. A single unaudited issuer, Tether, now carries over sixty per cent of the stablecoin market, and Tether and Circle between them hold close to the ninety per cent that Christine Lagarde attributed to two issuers in May, of a market she put at more than three hundred billion dollars. That concentration is not the footprint of a payment revolution reaching the unbanked of the pitch. It is the footprint of an exit, frictionless and unquestioning, from a rigged game.

Done properly, digitalisation would remove the need to trust that operator at all, because the money would settle itself and answer to no one. The dollar stablecoin does the precise reverse. It puts the middleman back at the centre, fuses in one unwatched pair of hands the roles a banking system is built to hold apart, the issuing, the holding of the reserve, the taking of its income and the power to freeze, and asks for the unquestioning faith its cash-out window depends on. So the charge against the stablecoins we actually have stands, and it stands at full force: they are fiat's dependence with fiat's safeguards torn off, built by the wrong hands for an audience that wants no questions asked, and carrying, by design, no one obliged to answer when they fail. Which returns us to the question this essay opened with, the one that decides everything after it: when it goes wrong, who answers for it?

Yet the instrument is not the villain, and this is the turn the rest of the essay is built on. On-chain fiat, real digital cash standing for the dollar or the pound or the franc, is the very thing that finishes the unbuilt second half and unlocks the efficiency the economy has left on the table for decades. The fault was never the form. It was the assurances discarded by choice and the roles fused without a watcher, and both of those are fixable. A representation of fiat that kept the assurances of bank money, audited, capitalised, supervised, answerable, with the right actors in the right places rather than a single cashier marking its own book, would be everything the pitch promised and nothing it has so far delivered. That is the unfinished business, and it is what the rest of this essay is about: not whether on-chain dollars should exist, for they should and they must, but how the same instrument, built by the right hands with its safeguards restored, becomes the thing it was always meant to be.

The trade that has to be honest

One principle governs everything that follows, and it is worth stating before the evidence, because it is the test every arrangement in this essay is put to - as it must be, and as I argue at length in the Internet of Economics Un-White Paper.

Trust is what buys efficiency. Trust without accountability is not trust at all; it is abuse waiting to happen.

A trusted ledger, run by an accountable operator, will always be faster and cheaper than a trustless one, and that is not a flaw to be engineered away. The bank's ledger is more efficient than any trustless blockchain, and it should be. What you may not do is take the efficiency of a trusted system and quietly discard the accountability that is supposed to come with the trust. That is the whole of the test, and it is either a fair exchange or a swindle: you may trade trustlessness away for efficiency, but only if you gain accountability in return. The stablecoin as it stands fails that test. It takes the efficiency of a private ledger, sheds the accountability of a supervised one, and keeps the difference for itself.

Let me be plain about where this essay stands, because it is easy to mistake for its opposite. It is not written against the banks. It is not a defence of fiat either, and on that I want to be exact. The argument is narrower and harder than either: an economy that wishes to keep its fiat currency will have to make that currency work for the digital economy now arriving, because AI and the machine economy will change everything, as surely as night follows day. One of the reasons the world needs the Gaju is to place a genuine discipline on monetary inflation, the slow debasement that has enslaved the majority and diminished the global economy for all.

This is also where the banks are most often misread, not least by themselves. What a bank sells is trusted convenience, and in a digitalised economy that becomes worth more, not less. Blockchain is the base of the digital economy now arriving and the real beginning of the transition from digitised claims to digitalised money, and it is a harsh mistress: it hands the user total responsibility and forgives no mistake. Most people will not want to carry that responsibility alone, and they will reach for an interface they already trust to carry it for them, which for the ordinary saver and the ordinary business means their bank. A bank's stock in trade is exactly this: trust, and the accountability that ought to come with it, a solvent and supervised institution that answers for the money. So the conclusion runs the opposite way to the one the banks fear: in a digitalised economy of the kind we propose, they stand to earn more, for less risk, than they do in the digitised economy they operate today.

The same logic governs how real-world assets come on-chain, and there it is plainer still. A real asset can be fully digitalised, made into a digital object that carries its own ownership and settles itself, only where binding law and real enforcement stand behind it, within the jurisdiction in which it is created and used. A Swiss building is a Swiss asset: who owns it, how it may be used, and what may be done with it are matters of Swiss law, Swiss regulation and Swiss enforcement, and no token alters that or stands outside it. Far from making the governed layer optional, this makes it indispensable. The chains that carry real assets must be governed, operating under the law of the jurisdiction whose assets they carry, because only law can make the claim on the chain and the right in the world one and the same thing.

Beneath all of it sits one neutral layer that no one owns and no one operates, carrying money no government can print: the Gaju, sound money by construction. The fiat each economy issues will compete with it, currency against sound money, and that competition is not a threat to be managed but a discipline to be welcomed, because it is the one check on monetary inflation that does not depend on the restraint of the people doing the printing. That is the shape of the whole argument. Work with the institutions that carry accountability rather than around them; separate the jobs the stablecoin has fused and reward each honestly for the risk it bears; govern the chains that carry real assets under real law; and leave beneath all of it a single neutral layer that answers to no one, so that the choice between the governed system and the ungoverned one disciplines the first without anyone's leave and, through that same layer, also serves it. Everything from here is the evidence for it, the central banks themselves, as we will see, having begun to make the same case in their own words.

The product is the float, and the holder is the bag

Look at the existing stablecoins the way you would look at any business, with the marketing stripped off. It is a bearer claim on a private company that holds a reserve, keeps the income that reserve earns, and keeps the right to freeze the claim in your hand. That is not an insult thrown at the industry. It is the business model, set out in the issuers' own filings. It is also the casino's economics seen from behind the cashier's window: the float is the house's standing take, and the reason holders accept an instrument built to extract from them is the one already given, that this is the only door the chips can leave by.

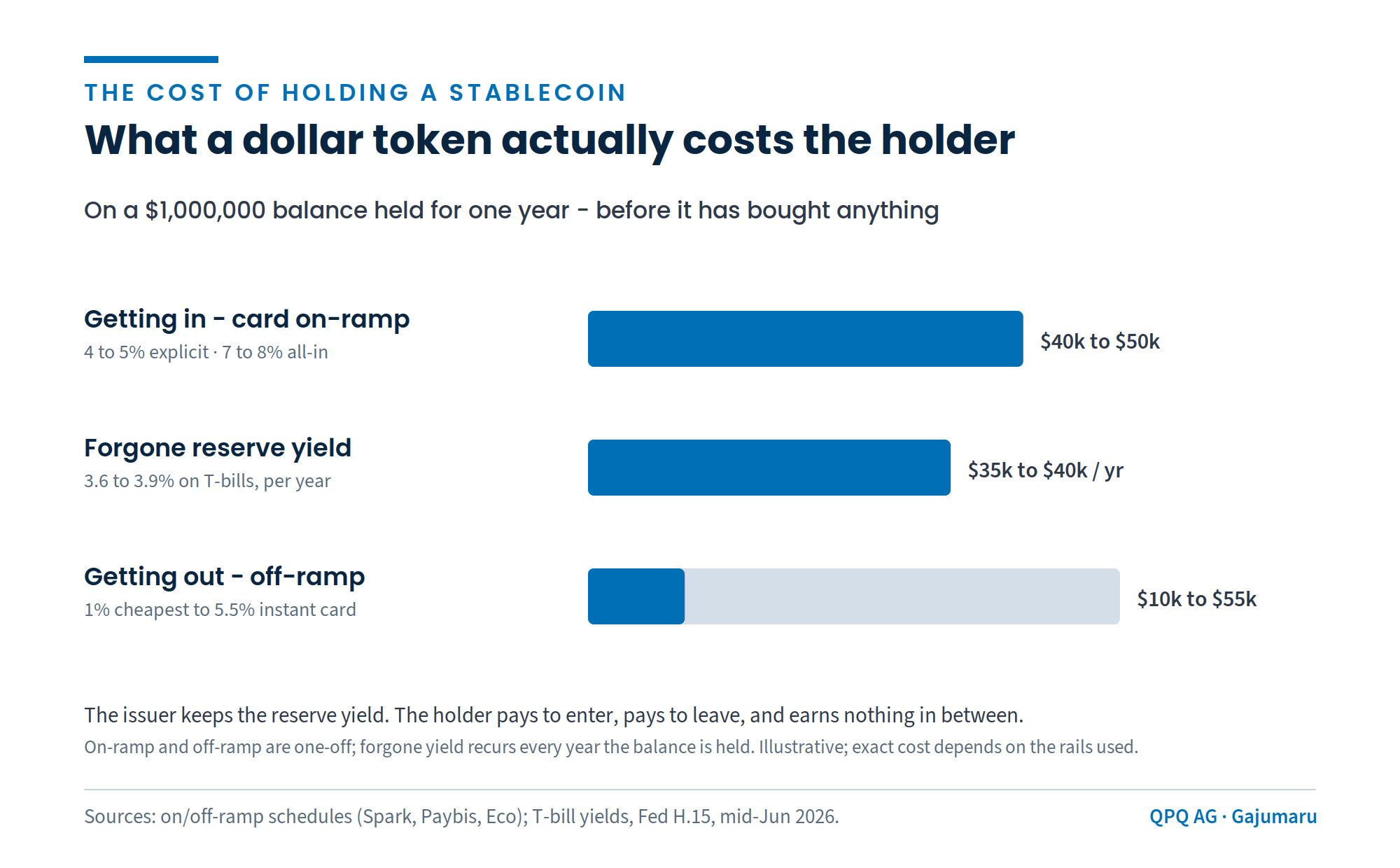

Tether earned more than ten billion dollars of net profit in 2025, on a staff of around three hundred people, and the holders of its coin saw none of the interest the reserve threw off. Circle is the same in shape, only more openly disclosed: in the last quarter of 2025, income on the reserve was seven hundred and thirty-three million dollars out of seven hundred and seventy million in total revenue, about ninety-five per cent of everything the company took in, and its largest distribution partner is paid the entire reserve income on coin held through that platform. The yield on the reserve is the product. The coin is the device that takes that yield from the person whose money funds the reserve and hands it to the person who issued the claim.

The holder pays twice more besides giving up that yield. Getting in costs four to five per cent on a card, nearer seven or eight once the spread is counted; getting out runs from about one per cent at the cheapest to five and a half for an instant card withdrawal. The interest given up is not small either. With short-dated United States Treasury yields between roughly three and six-tenths and three and nine-tenths per cent in the middle of June 2026, a million dollars left sitting in a stablecoin that pays nothing hands the issuer something like thirty-five to forty thousand dollars a year that would otherwise have been the holder's.

Then there is the freeze, and behind the freeze the question of whether the issuer is good for the money at all. Tether can freeze any balance at will. As for the reserve, the case the industry would rather you forgot is March 2023. Circle disclosed that three point three billion dollars of USDC reserves, about eight per cent of the whole, were sitting in Silicon Valley Bank as it failed; the coin dropped to around eighty-seven cents and stayed below its promised dollar all weekend, while the big exchanges simply switched conversions off. The promise of par held for exactly as long as confidence in the reserve held, which is to say it held until the moment it was tested. This is the BIS point made flesh before the BIS made it: par "disintegrates when stress hits."

When does a stablecoin actually settle?

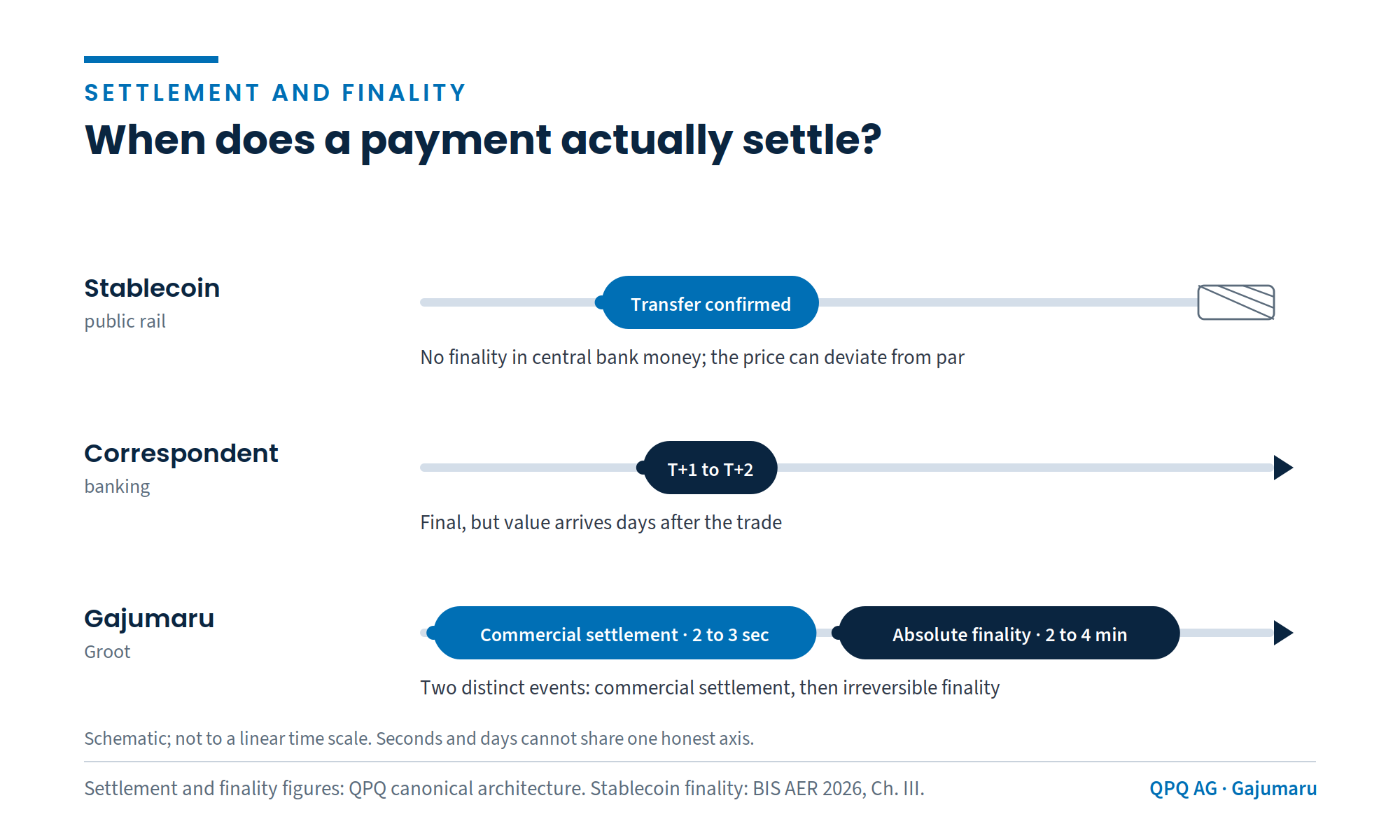

Set the issuer's credit aside for a moment and ask the two questions the whole structure turns on: what is settlement, and what is finality? They are not the same thing, though they are run together so often, and usually so harmlessly, that the difference has worn away. Settlement is an economic calculation: the point at which reversing a transaction has become irrational, because the cost of undoing it now outweighs anything undoing it could gain. It is probabilistic and continuous, it rises with the value at stake and the certainty accumulated above it, and it has no fixed endpoint, because it never makes reversal impossible, only pointless. Finality is something else: the point at which reversal is not merely irrational but structurally impossible, by any means, whatever the resources or the intent of whoever attempts it. Every payment system has settlement of a kind. Almost none has finality.

The reason the difference can be ignored most of the time is that at the level money is normally handled, between central and commercial banks, the two genuinely coincide. When value settles in central bank money, or settles as a balance a solvent and supervised bank owes you, every assurance is already in place and the matter is closed, about as closed as anything denominated in a currency you hold by permission can ever be. There, settlement and finality are one word for one event, and the BIS, working at exactly that level, treats them so. The equivalence is real, and it is precisely what the stablecoin borrows without earning.

Take a stablecoin payment and the two come apart again, with only the first delivered. Trading Ether for the dollar token settles: the trade executes on-chain, the position moves from one holder to the next, and within seconds undoing it is irrational. But that is the leg inside the system, and the token goes no further. The BIS says as much in its own terms. These transfers "settle neither directly nor indirectly on central bank balance sheets," because no central bank money ever enters them, and what passes between the parties is a private company's liability whose price drifts off par, which is why the BIS places these instruments closer to "exchange-traded fund shares rather than a means of payment." An ETF share is a perfectly good thing to own. It trades; it does not close the account. Holding a price is not being final, because a price is the market's opinion from one moment to the next, and finality is the end of opinion.

Finality, for the holder of the token, lives one crossing further on, and it is the crossing they still have to make: the dollar token redeemed for fiat in a supervised bank's ledger, par against every other dollar, drawable on reasonable notice as the physical cash this essay began with, the bearer object that closes an account with no question asked. That is the leg that ends the exposure, the one at which settlement and finality finally meet again, and it is exactly the one the stablecoin defers and taxes at both ends. Even there the finality is the qualified kind, final only so far as anything held by permission is ever final, because a balance a third party can freeze is never wholly closed. But set that qualified, genuine finality beside what the token actually delivers, a settled position in a private claim that has crossed nothing, and the distance between the two is the whole story.

Odd as it seems, the story of today's stablecoins is not a new one. It is the story of every economy shut out of the system, adapting to what it cannot change. Sixteen years ago I met with a number of money dealers in Johannesburg and Pretoria. Their trade was simple: they bought the US dollars sitting in your Zimbabwean bank account, after the hyperinflation farce had run its course, and paid you in physical US dollars. For every dollar you transferred to them inside the Zimbabwean banking system, they handed back, at most, twenty-five cents in cash. You needed a million dollars to pay for a grain shipment so people could eat? No problem. Transfer four million to one of them within the Zimbabwean system, and the cash was yours.

Immoral? Carefully, I have to say no. When I began in asset management twenty-five years ago, I learned that the most fundamental tool in price discovery is to locate risk exactly: its moment, its place, and its size. The dealer I knew best, holding court in the Mug & Bean in Bedfordview with a troop working the phones around him, had a problem of precisely that kind. The cash he handed across the table was final the instant it changed hands; possession was settlement and finality at once. What he took in return was not money but a risk, the risk of getting the dollars that now sat on his ledger inside Zimbabwe back out as dollars he controlled. That was no small undertaking. It meant navigating Zimbabwean currency controls and waiting in the queue to draw on the bank's meagre balances in its New York vostro account, time and management both, until the position was unwound and he had finality of his own: dollars in cash, or dollars in a US account he held. The discount was the price of carrying that risk, and he stated it openly.

The issuers, USDT, USDC and USD1, differ in one decisive respect. They never take the risk. They take your bank-grade dollars and hand you a token that is a claim on unaudited, unsupervised reserves, a claim you must simply trust, carrying all the risk and meeting none of the accountability, that when you come to call on those reserves they will be there. The dealer in the Mug & Bean did the opposite. The man who transferred a million dollars from his Zimbabwean account walked out with a quarter of a million in cash, final and his, and a decent canvas bag thrown in for free.

The liability and the rail

The questions of credit and of finality still leave something out, and it survives a perfect reserve. A coin can be backed to the last cent in Treasury bills, redeemable at par, audited and licensed, everything its defenders ask of it, and still seize up. The reason is not the asset. It is the rail the asset rides on. The sharpest statement of this comes from inside the Federal Reserve itself, in a paper published on the second of June by economists at the Board.

The paper pulls trust into two pieces. The safety of the asset is one question; the rail it moves on is another, and on a permissionless chain the rail is priced one transaction at a time, by how many strangers want space in the same block at the same instant, almost none of them there for the coin you are sending. Two forces pull against each other: the network effect, which makes a money more useful the more people hold it, and the congestion cost, which climbs as the chain fills. As a coin's use thins and the chain around it congests, cashing out becomes what the paper calls a strategic complement, a precise term for a stampede: every holder who leaves pushes the cost up and the usefulness down for those who stay, and hands the next a sharper reason to leave. Measured, it is not a smooth response to rising fees but a sudden break, bunched in the worst moments of congestion, the signature of a run.

Putting Fedwire's 2021 volume across Ethereum would have cost around seven and a half billion dollars against the hundred and seventy-two million Fedwire charged, more than forty times as much and far more erratic. When the break does come, holders abandon the rail, not the coin, the paper tracking Tether's balances crossing off Ethereum onto Tron and its circulation shifting to Solana. The coin is sound only by assumption here, and the assumption earns no free pass, because the reserve behind a real stablecoin has a depth and a timing to its liquidity that may not meet a wall of redemptions. What the data shows is the rail giving way, and giving way first: the stampede empties the chain of capacity before the reserve is ever called, so the claim is never put to the test at all.

The paper leaves two distinctions undrawn. The first is that the run is a property of low-capacity chains, not of permissionless chains as a class. The chains the paper speaks of settle almost nothing. Ethereum's base layer carries fifteen to twenty-two transactions a second; Solana, which markets sixty-five thousand, settled around two hundred and fifty under real load when demand arrived in the memecoin surge of April 2024, with more than three-quarters of its non-vote transactions failing on the chain; and the Layer 2s built to relieve Ethereum share a single budget of data space per block, so that a rollup advertising forty thousand transactions a second is measured by L2Beat in the tens. The run bites because the room is tiny and shared, so a dollar token competes for the same block as unrelated speculation and is priced out when that speculation surges. Put the same money on a chain with room of its own and the mechanism has nothing to feed on.

The second distinction is that pricing a rail by who will pay most for priority is not the flaw the paper takes it for. It is the ordinary course of business, the price signal that drives incentives to fulfil it. A bank charges more to settle a transfer instantly than to clear it overnight, and nobody calls that fragility, because the capacity is there and the premium buys a place in the queue rather than the survival of the queue. The fragility is not that the rail charges for priority. It is that the rail has so little room, shared with traffic that has nothing to do with the coin, that ordinary value is forced out in a stampede, and that no one stands behind the rail to answer when it does. Strip the legitimate part away and the diagnosis narrows to its true terms: low capacity, shared congestion, and no one accountable.

None of this stops at stablecoins. The same mechanism reaches a tokenised bank deposit, a tokenised Treasury bill, even a central bank digital currency, if any of them is issued on a congested permissionless chain. A safe liability on a fragile rail remains a fragile instrument.

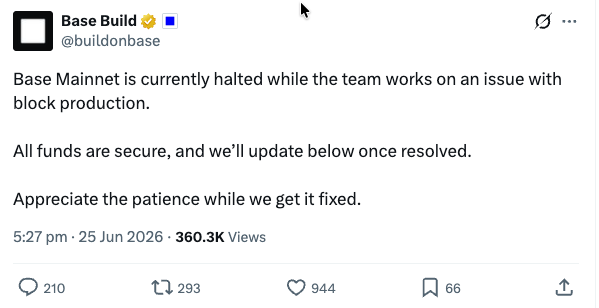

Then the paper reaches for a cure. It proposes a chain the central bank runs itself, or a chain built for the single application, or a trusted Layer 2 that, in its own words, would likely require "some degree of centralization," run by something close to a central counterparty. The authors reached for a Layer 2 because it is the instrument in front of them, exactly as the BIS reached for a permissioned ledger run by central banks: each names the cure its own frame allows. But the Layer 2 will not bear the weight. It is not "some degree" of centralisation; it is the whole of it. A single sequencer orders every transaction and can include, delay, reorder or exclude any of them at will, with no proof behind the choice and no way to remove the operator. The largest, Base, runs one sequencer operated by Coinbase, a company listed on NASDAQ, authorised under MiCA in Luxembourg and registered with FinCEN, and that sequencer sits outside every one of those regimes because the activity has not been classified. If a Layer 2 were the critical market infrastructure the paper's cure would make of it, it would have to be far more robust than Base has shown itself to be. Base has gone dark twice: for twenty-nine minutes in August 2025, and for roughly two hours on the twenty-fifth of June 2026, the cause given only as an "invalid block" and the root of it undisclosed both times.

What halts when Base halts is the cash-out rail itself: USDC, the dollar token at the centre of this argument, settles natively on Base, so the second outage shut the exit for those dollars for two hours, on the day Bitcoin fell to a multi-year low and holders most needed it. A settlement layer that stops under stress, takes the cash-out rail down with it, and will not say why is not infrastructure in any sense a banking supervisor would accept, and the convenience is that nothing serious follows when it fails. For the supervisor who wants to understand what a Layer 2 actually is, the mechanics are set out here. The Fed's safe rail is a single identified operator controlling a financial network of that size while the supervisors apply none of the rules their own doctrine of substance over form already hands them.

Set the Layer 2 aside, and the paper reached for something else in the same breath: a chain built for one purpose, on room of its own, with someone who answers for it. That is the cure. The paper pointed past the problem it had diagnosed to the restoration itself, then stopped one step short, because the other half of the answer sits outside the frame a Fed paper can hold. The choice it draws, a rail permissionless and fragile or a rail safe because someone has been put back in charge of it, is a false one. There is a third thing the frame had no room to name: the accountable rail the paper reached for, and beneath it a neutral ground that no one owns.

The regulators converge, and one of them goes to war on two fronts

Governments have noticed uniformly, across jurisdictions that agree on almost nothing else.

The United States passed the GENIUS Act, signed into law on the eighteenth of July 2025: payment stablecoins must be backed entirely by high-quality liquid assets, the issuer must be licensed, and the issuer is barred from paying any yield to the people who hold the coin.

Europe's Markets in Crypto-Assets regulation controls stablecoins venue by venue under its Title V, and the effect is already visible: Tether's coin was taken off European Union-regulated venues, by Coinbase in December 2024 and by Binance on the thirty-first of March 2025; the larger tokens must hold at least sixty per cent of their reserves as bank deposits; and the window in which crypto firms could operate under transitional arrangements closes on the first of July 2026. That deadline caught the largest exchange of all. Binance withdrew its Greek licence application on the twenty-fourth of June 2026, holds authorisation in no member state, and from the first of July cannot serve clients anywhere in the bloc; some two hundred firms cleared the bar that it did not. The licence turns on questions a passport cannot dodge: the regulator's reported scrutiny of Changpeng Zhao's continuing influence as an owner after his removal from management, and a fitness test that reaches effective control and qualifying shareholders rather than titles. An exchange built so that no one jurisdiction can quite say who controls it is an exchange that struggles to be authorised by a regime that requires exactly that answer. The European Transfer of Funds Regulation has been enforceable since the thirtieth of December 2024, with no grace period and a rule that the identity of both parties travels with every transfer. Japan has required registered, fully-reserved issuance since 2023.

Beneath the convergence, the American settlement is the site of an open fight the other jurisdictions have not yet had. The GENIUS Act drew one line clearly: the issuer may not pay interest to the people who hold the coin. The Clarity Act, still working its way through the Senate against a crowded calendar, carries wording the banking industry reads as a way around that line, one that would let a crypto exchange, rather than the issuer, pay stablecoin "rewards," which is interest under another name. The banks are vehemently opposed, and the most senior banker in America has not been diplomatic about it. Jamie Dimon, who runs JPMorgan, told Fox Business that the arrangement "allows them to effectively pay interest on deposits, stablecoins, or something like that, without the protection that they should have," that it has "almost no legal protections, so no, the banks will not accept it that way," and that were it to pass he would have nothing to do with it and it "would eventually blow up on its own." His objection is to the asymmetry rather than to the instrument: a firm that takes deposits like a bank, he said, "should have bank rules."

The contempt was aimed at Coinbase's chief executive, Brian Armstrong, who has led the push for the provision. Armstrong, Dimon said, is the only one who wants it and is spending hundreds of millions of dollars in Washington to get it; told that Armstrong claims to speak for the whole industry, Dimon answered that Armstrong was "full of s**t." Coinbase helped create the USDC stablecoin and, though no longer in its governance, still earns a large income from it, because the issuer, Circle, pays Coinbase on the balances held through its platform. In the first quarter of 2026 Coinbase's revenue fell by more than six hundred million dollars year on year, it posted a net loss of three hundred and ninety-four million and it cut staff; stablecoins brought in around a hundred and ninety-two million in net revenue, without which the loss would have been close to six hundred million. For a business shaped like that, a rule about who may pay yield is the difference between the model working and the model failing. The other side reads the whole quarrel as incumbents defending their turf, and argues the rules belong to lawmakers rather than to the banks that stand to lose; the economist Peter Schiff, no ally of the banks, called Dimon's demand that issuers be regulated like banks nonsense.

The shape of the legislation is easier to read once the money behind it is on the table, and the scale of that money is a matter of record. In the 2024 cycle crypto corporations put around a hundred and nineteen million dollars into United States federal elections, by Public Citizen's count from Federal Election Commission data, close to half of all corporate money spent that cycle, ahead of oil and ahead of the banks. The industry's main vehicle, the Fairshake super political action committee, raised on the order of two hundred million dollars and spent more than a hundred and thirty-five million, the large majority of it straight from corporate treasuries. The spending was deliberately bipartisan, run through two affiliates with one aimed at each party, which marks the money as corporatist rather than partisan: it backed and attacked candidates of both parties to a single end, a Congress disposed to write the rules the industry wanted. At the inauguration the same firms gave at least ten million dollars to the fund, Ripple five million in its own token, Robinhood two million, Coinbase, Kraken and Circle a million apiece. None of this is unlawful and none of it is concealed. It is the price of shaping the rules, paid in the open.

One venture sits closer to the centre than any other, and it is a stablecoin. USD1 is issued by World Liberty Financial, the digital-asset company of the President's family; the company lists him as co-founder emeritus and his three sons as co-founders, and it is owned in part by a family entity, DT Marks DEFI LLC. Its own disclosures show that seventy-five per cent of the proceeds of its token sales flow to that entity, and a Reuters investigation estimated the family had earned at least two and a third billion dollars across its crypto ventures. The reserve income, the float this essay has followed from the start, accrues to the issuer and not to the holder. USD1 was the asset in which an Abu Dhabi state vehicle settled a two-billion-dollar investment in Binance. The mechanism set out at the start, a private issuer keeping the yield on the dollars behind a token, here keeps that yield for the family of the man who signs the laws that govern it.

Beside that runs a second record, of pardons. Changpeng Zhao, the founder of Binance, had pleaded guilty to failures under the Bank Secrecy Act, the United States anti-money-laundering statute; he was pardoned in October 2025. The founders of BitMEX, and the operating company itself, had pleaded guilty to the same class of offence; they were pardoned in March 2025 and a hundred-million-dollar corporate fine fell away. The Clarity Act has stalled in the Senate in part over how to handle the President's financial ties to the venture, with members of both parties pressing for ethics provisions, while the White House holds that the previous administration was simply too harsh on the industry. These are the events, dated and on the record. For a very much more entertaining review of it all, I would direct the reader here: https://gothburz.substack.com/p/these-events-are-unrelated.

Dimon was blunter still on the laundering risk. Banks must verify who sends and who receives; a stablecoin, once it leaves a regulated institution, can pass from wallet to wallet, so that "the first one may be legitimate, second one may be a sex trafficker," and "if they don't do it thoughtfully, it will be a huge problem." That is the rail with no one to serve a subpoena on, described from inside the largest bank in the country. Dimon is no enemy of the instrument, either: he said plainly that he expects stablecoins to be used for cross-border payments and small-dollar transfers between people, the same narrow and genuine uses this essay granted at the outset. His quarrel, and the banking industry's, is not that on-chain dollars should not exist, but that a thing which takes deposits and moves money the way a bank does cannot be let do so without a bank's assurances and a bank's supervision. The fight over the rewards provision is the fight over whether the wall comes back or stays down, and the party arguing to rebuild it is the regulated banking system itself.

The Bank of England moved most recently, on the twenty-second of June, with a policy statement and a draft Code of Practice for systemic stablecoins. The Bank did not impose a holding limit. It consulted on one and then dropped it, and put in its place a temporary cap on issuance of forty billion pounds per systemic coin, openly for the purpose of protecting the supply of credit, with backing of seventy per cent short-term United Kingdom government debt and thirty per cent central bank deposits, the regime live from 2027, with the Financial Conduct Authority supervising the coins that are not systemic.

The common thread is the same across every regime: full reserves, a licensed issuer, and an anxiety about what all of this does to bank deposits. The United States Treasury's own advisory council has put roughly six point six trillion dollars of transactional deposits in the category it calls "at risk"; Citigroup projects between one hundred and eighty-two and nine hundred and eight billion dollars of deposits displaced by 2030; and the Federal Reserve's own modelling produces a contraction in bank lending somewhere between sixty-five billion and one point two six trillion dollars, depending on the scenario.

Inside that convergence, the European Central Bank has taken a position of its own. The ECB is fighting a war on two fronts at once. With one hand it is driving private stablecoins out of regulated venues through MiCA. With the other it is building a state alternative, a retail digital euro, and the design of that instrument is the tell. The ECB's own closing report on the preparation phase, from October 2025, sets the holding limit for the digital euro somewhere between five hundred and three thousand euro per person, with possible issuance around 2029, and pairs that cap with no interest paid on the holding, the two features together tuned precisely to keep money from draining out of the banks. The bank has written its own diagnosis into the design. It is capping how much of its own money a citizen is allowed to hold, and refusing to pay interest on it, for one reason: it knows that central bank money in the public's hands, uncapped and paying interest, would pull deposits straight out of the banking system. The holding limit is the ECB's own admission, set down in its own instrument, that the thing it is building threatens the very deposit base it is trying to shield from stablecoins.

What makes the European stance singular rather than merely strict is the contrast with the United States, which went the opposite way on both questions in a single motion. An executive order in January 2025 forbade a United States central bank digital currency while actively promoting dollar-backed stablecoins, and on the twenty-second of June 2026 the Senate passed, by eighty-five votes to five, a housing bill carrying a four-year ban on a digital dollar that runs to the end of 2030, now waiting on the House and the President's signature to become law. One bloc bans the state coin and clears the field for the private dollar; the other expels the private coin and builds a capped state coin of its own. Europe alone is doing both at the same time, and the question it has not answered is the one its own digital euro design quietly puts on the table: if uncapped central bank money would drain the banks, and private stablecoins would drain them too, what is the plan for the banks?

Singleness, and the institutional ledgers that miss the point

Behind the worry about deposits sits a deeper one. In her address of the eighth of May, Lagarde put the stakes where they belong, on the singleness of money itself. A settlement layer built on private stablecoins, she warned, risks leaving Europe with "multiple platforms and no common anchor for convertibility," and a Eurosystem survey has already found that the absence of a widely accepted tokenised cash settlement asset is holding tokenisation back across Europe. The ECB is measuring the problem now, and acting on it. Pontes, live from September 2026, links distributed-ledger platforms to TARGET so that transactions on those ledgers settle in central bank money, building on tests in 2024 that ran fifty transactions across nine jurisdictions and settled around one point six billion euro; and the Appia roadmap, published in March 2026, lays out a path to a fully interoperable European tokenised financial system by 2028. On the instrument itself the ECB is cool towards euro stablecoins, which come to perhaps five hundred million euro in total, a rounding error beside the dollar coins, and leans instead towards tokenised deposits, with Isabel Schnabel arguing in her address of the first of June that the right course is to separate the instrument from the technology beneath it and to keep the tokenised system "open and multi-currency in nature."

What these two are asking for is one thing, but they don't yet know what it is or that its base exists. Lagarde titled her address "separating functions from instruments"; Schnabel's whole argument is that the instrument must be prised apart from the technology beneath it. The principle is functional separation, the unbundling of the jobs that money does so that each can be supervised and provided on its own terms, and it is precisely the principle the bundled institutional ledgers violate.

The BIS chapter backs every part of this and sharpens it. Money is accepted with no questions asked, it argues, because there is a common unit of account and the singleness that follows from it: par, redeemable in central bank money, with finality, held up by central bank liquidity that can stretch to meet demand. Take the common anchor away and the structure does not bend, it breaks. A coin on the Ethereum ledger is not the same thing as a coin of the same name on the Solana ledger, and this splitting across chains "can undermine the singleness of money in the absence of an agreed clearing and settlement system across ledgers." Two tokens that share a name with no guarantee of par between them are not money. They are a set of private claims wearing the same label.

The answers came quickly, and they were opportunistic. Each is a governed ledger in the dress of decentralisation, and the serious institutions drawn in behind them lend it a credibility its own design has not earned.

Take Canton, the most serious of them. Its Global Synchronizer, the part of the system that puts transactions in order and keeps the network running, is operated by a permissioned set of Super Validators, admitted by invitation and supermajority and voting as equals; the rules and the economic parameters are changed by a two-thirds supermajority through the Canton Improvement Proposal process; and every participant has to trust the synchroniser to order its transactions and keep the lights on. It is backed by serious institutions, Goldman Sachs, the Depository Trust and Clearing Corporation and Visa among them, and Digital Asset raised one hundred and thirty-five million dollars for it in June 2025. The Global Layer 1 initiative convened by the Monetary Authority of Singapore is a single-tier governed shared ledger, with a core group of BNY, Citi, JPMorgan, MUFG and SG-FORGE, since joined by HSBC and Euroclear, and watched by the ECB, the Banque de France and the IMF; its best and most lasting contribution is the standards work. Circle has launched a Layer 1 of its own, called Arc, and Swift's shared-ledger prototype runs on Hyperledger Besu with Swift itself operating the ledger.

What these designs share, the BIS has a phrase for. Permissioned networks, it warns, risk becoming "walled gardens that limit competition and innovation." The instrument for testing them is the one the late Tony Benn left us. Benn sat in the British Parliament for half a century and served in the Cabinets of Harold Wilson and James Callaghan; his politics were of the democratic left, and the five questions he taught are nonetheless the sharpest tool there is for testing unaccountable power, whatever language it dresses itself in. What power have you got? Where did you get it from? In whose interest do you exercise it? To whom are you accountable? Last, and the one that matters most here: how do we get rid of you? Put those five questions to the operator of a synchroniser, or to the governing cohort of a shared ledger, and the answers come back describing a controller sitting in a position of trust. If the participants cannot remove the people who order their transactions, the network is not decentralised. It is centralised infrastructure wearing decentralised branding, and the price of that arrangement is exactly the worst of both worlds the BIS warns against: the users carry the costs of the distributed form while the operator slips the accountability that ought to come with the control it actually holds.

These designs keep the governance and throw away the neutrality. Not one is neutral ground, and not one provides a common anchor that holds across jurisdictions rather than inside a single one. The BIS concedes it in the middle of making its own prescription: across jurisdictions "there is no single unit of account and no universal settlement asset," and singleness is therefore reached "within each currency, not universally." Every governed ledger can hold singleness together inside its own walls. Not one can hold it together across the wall, between rival jurisdictions that will never submit to a shared operator. That is the unsolved problem.

The mirage, and the prize that is actually at stake

Before the architecture, one piece of arithmetic has to be cleared off the table, because it distorts the entire debate. The headline transaction figures for stablecoins are a mirage.

McKinsey did the work of separating the headline from the substance in February. Reported stablecoin volume runs as high as thirty-five trillion dollars a year. Actual payments by actual end users come to about three hundred and ninety billion dollars a year, roughly two-hundredths of one per cent of global payments. Inside that real figure, business-to-business payments are about two hundred and twenty-six billion, around sixty per cent of all stablecoin payments, and grew seven hundred and thirty-three per cent in a year; remittances and payroll add about ninety billion, under one per cent of their categories; capital-markets settlement is about eight billion, under one-hundredth of one per cent; and stablecoin-linked card spending is about four and a half billion. The growth rates are real and large. The base is still tiny. The gap between thirty-five trillion of reported volume and three hundred and ninety billion of genuine payment is the gap between activity and self-dealing.

The BIS, with its own data, puts a number on the self-dealing. Stablecoin transaction volume was about twenty-eight trillion dollars across 2025, which, it notes, is "less than three business weeks of settlement volumes of the largest United States wholesale payment systems," and is far lower again once the self-dealing is netted out; the market capitalisation stood at about three hundred and twenty billion dollars at the end of May 2026; and ninety-nine point four per cent of fiat-backed stablecoins are pegged to the dollar. The whole sector, measured as a settlement system, clears in a full year not much more than the largest United States wholesale rails clear in three weeks of business. Most of the volume is the market settling its own bets, the casino window of the opening now in figures, and the thin sliver that is real payment is the measure of how little of the promised digitalisation the instrument has delivered.

The threat to the banks is not the payment volume but the deposit base: not the flow across the rail but the stock of deposits that could move to fund the reserves behind the coins. All three of the BIS's reserve scenarios begin with a weakening of the banking sector's funding position; stable retail deposits give way to concentrated, rate-sensitive wholesale deposits; the liquidity measures worsen; and credit to small and medium-sized firms through the smaller banks could suffer. The net effect on the wider economy, even at a scale of one to three trillion dollars, it judges to be negative but "quantitatively modest," because banks adapt and defend their ground and competition can work in the customer's favour. The risk is structural rather than apocalyptic, and the question is who ends up holding the float, and whether the deposit base stays inside the regulated system or drains into private hands that keep the yield.

There is one more cost, and the BIS names it. Stablecoins account for a significant share of illicit activity on-chain; the pseudonymity of the wallets and the use of unhosted ones undercut the anti-money-laundering and know-your-customer controls the rest of the financial system is held to; and mixers and bridges are used to hide where the money goes. It is the accountability problem again: where there is no one to answer for the money, there is no one to ask.

What we built, and why it answers the diagnosis

Everything to this point has been, almost word for word, the regulators' case and the central banks' own. The diagnosis is theirs; what follows is ours, built to answer it, squarely.

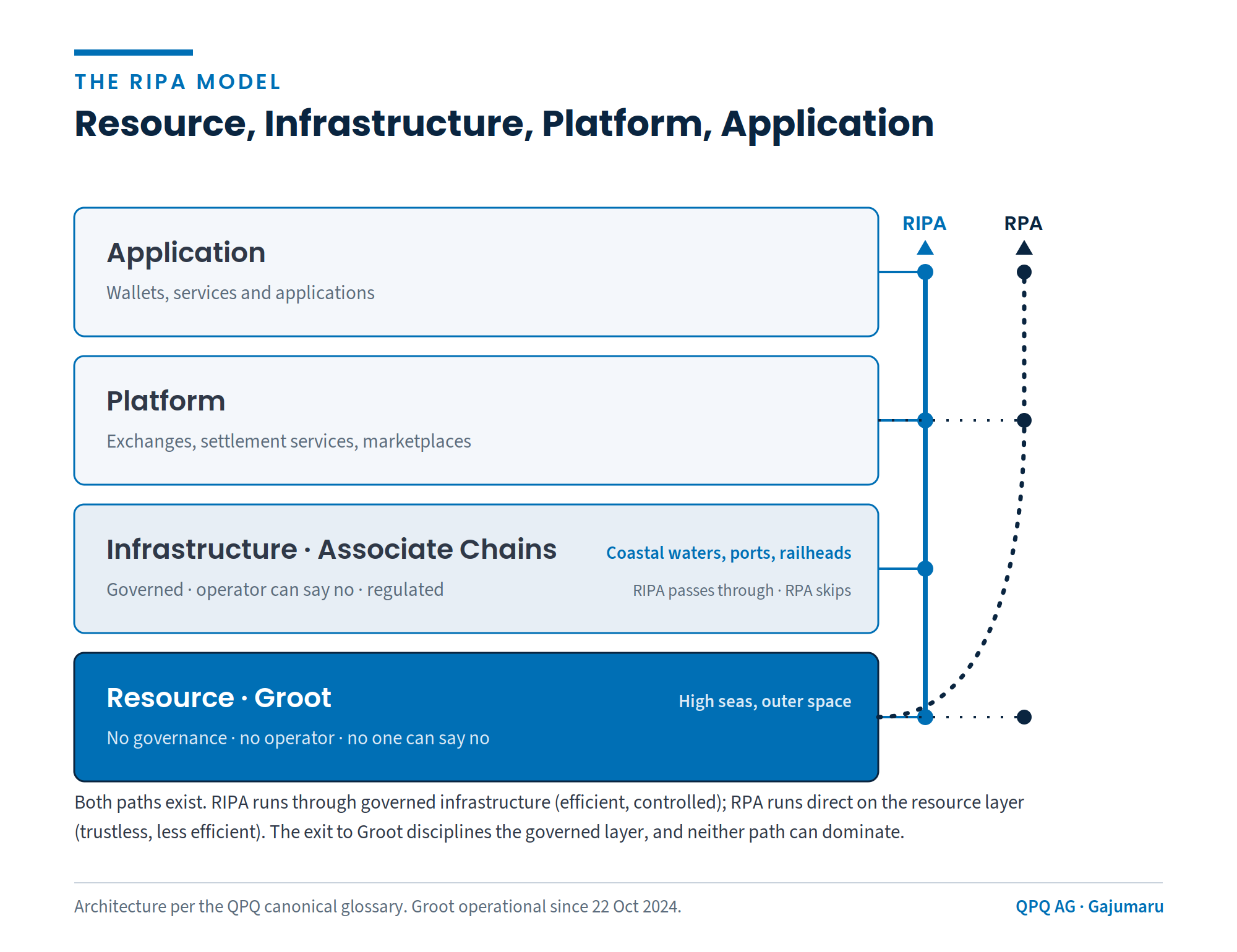

Everything else rests on the distinction between a resource and infrastructure. Groot is a governance-free proof-of-work resource layer. It has no owner and no operator; it has been live since the twenty-second of October 2024; and it carries more than three hundred transactions a second, settling in two to three seconds and reaching finality in two to four minutes. Its chain is kept within consumer-device capability by design, through trash collection and database minimisation; it may grow to something on the order of a hundred gigabytes, and what can be said with certainty is not a fixed ceiling but that it stays small enough for an ordinary machine to hold. A chain whose history grows without limit, as most do on the assumption of infinite library capacity that nobody else will notice, eventually passes beyond ordinary hardware and into the hands of those who can afford the storage, which is centralisation by another name. Groot is built so that it never does, and decentralisation stays wide and lasting. Its security is funded at first by issuance on a Fibonacci curve, which spreads the coin widely and lets the transaction fee stay low, and as the network is used that fee revenue grows until it overtakes the issuance, within five to twenty years depending on adoption, and carries the security from then on. It is not the efficient layer and was never meant to be: trust is what buys efficiency, and a trusted ledger will always be faster and cheaper than a trustless one. That is not the job Groot is for. Groot is the neutral ground beneath the governed ledgers, the one layer no jurisdiction operates and none can capture, the place where parties who share no common framework and no reason to trust each other can still meet and transact. Its worth is not its speed but that it is the single layer with no one on it who can say no, which is what makes it the exit that disciplines everything built above it. An exit of that kind does not have to match the efficiency of the governed system it sits beneath. It has to exist, and it has to be usable, and Groot is both.

The whole shape is the answer to the functional separation the central banks have been reaching for. Four layers, not one: resource, infrastructure, platform, application. The resource is Groot, the layer with no operator. Above it sits the infrastructure, the governed chains, in two families: currency chains that issue fully-reserved money, and securities chains that give tokenised shares and assets the enforceability of a domestic legal system. Above those sit the platforms and the applications that ordinary users touch. These governed chains answer for themselves, each operated and under its own jurisdiction's law, and Groot beneath them answers to no one; they are accountable instruments standing on neutral ground. This is the separation of functions made structural, the jobs the stablecoin fused, issuing the money, holding the reserve, earning its income, ordering the transactions and freezing balances, prised back apart so that each can be supervised on its own terms. Each is then rewarded for what it actually provides, the bank for the assurance it carries, the resource layer for nothing at all, because there is no one there to pay. The separation does a second thing the bundled designs cannot. The layer beneath is ungoverned and usable, so a party always keeps the choice to step off the governed infrastructure and work on the bare resource instead, less efficiently, but answerable to no operator, and that standing choice is the discipline. An infrastructure that extracts too much, or refuses too readily, loses its users to the layer below it, so the exit holds the governed system honest without anyone having to regulate it into honesty.

On that resource layer sit the governed currency chains that we are proposing for the world's leading banks and regulators to consider. We are working on the token specifications now and will work to engage those very same banks and regulators to deploy the first examples in 2027. Each currency chain is founded by a consortium of the banks that use it, who own the reserve pool between them. The pool is their own liquidity, run as a bank runs the deposits behind its current accounts, and they earn from it in more than one way. One issuer of record per currency holds singleness together directly: every token on the chain is a claim on a single reserve pool, par against every other, which is the thing the ECB says is missing and the thing the BIS says fragments across rival ledgers.

This is the stablecoin trap turned inside out, and the difference begins with the holder. A stablecoin is built so that getting out of it is hard, and the friction is the point: people leave large balances sitting in the token and give up the yield on the whole sum for as long as it sits. Here there is no such friction, because the customer's own bank is on the chain. The savings stay in the interest-bearing deposit, earning, and only a working balance is swept into the digital currency at the moment it is needed and back to fiat on deposit the moment it is not, so the customer gives up the yield only on what is in flight, which is small and brief. On the bank's side, the pool of balances behind the currency is a liquidity pool, the working money that funds the currency in motion, distinct from the bank's longer-term treasury holdings, and the bank pays nothing on it because the currency is a tool, not a deposit, exactly as a bank treats the float behind its current accounts.

The reserve yield on that pool is not new money but the same income, kept by the bank that carries the customer rather than by an issuer that carries none, and the bank earns it at very low risk and against almost no regulatory capital while the deposits, the customer and the settlement all stay inside the regulated system. The inducement is plain: a bank that earns on the money moving across a chain it owns has every reason to bring that money onto it, rather than watch it walk out of the door to a private issuer. This is the heart of it. The purpose of the Gajumaru is not only to discipline power by creating a real choice between trustless and trusted, between fiat and sound money. It is to value every necessary part of the system, giving each component the incentive to provide its service and the user a genuine choice to value it. It removes the frictions that tax both the user and the provider, so that the choice is rent-free and true. Our object is not the destruction of the banking system, which is arguably where the current stablecoins lead, hollowing it out and leaving the world with fiat's failings and none of its assurances, but to save it: handing the regulated system, at the infrastructure layer, the tools that value every part the stablecoin discards, while Groot beneath supplies the freedom and the Gaju the soundness that keep it honest. This is a model for the regulated banking system and the customers inside it. Beneath it, Groot is already open to anyone the fiat system excludes who is willing to transact in the open, in Gajus, on a public ledger that anyone can see. What that leaves to the stablecoins is the remainder: the demand that wants a dollar token and wants its activity unseen, for which a transparent public chain is not a missing door but the very thing to be avoided. That is the ground we are not setting out to contest, and are content to leave where it is.

A working digital currency earns its place by what it makes possible, and the securities chains are where it shows. A nation that puts its assets and its money on chains of its own can settle the one against the other directly: a tokenised asset on a securities chain against the domestic currency on a currency chain, in its own currency, with no settlement risk between the two. That is the benefit a fully-reserved digital currency is for.

On Groot, commercial settlement completes in under three seconds, in a microblock; absolute finality, the kind that cannot be reversed, follows in two to four minutes, with the second keyblock. These are two different things, and the difference between them is the substance; folding them into one reassuring number is the very sleight the stablecoin works. A merchant has commercial settlement in seconds, enough to hand over the goods, because by then the cost of reversing the transaction already runs past anything to be gained by reversing it; a central counterparty closing its books waits the few minutes for the finality that cannot be undone. The stablecoin rail never reaches finality in central bank money at all, and is priced by congestion at every step along the way.

The rail is the harder charge, and the architecture answers the Federal Reserve directly. The result needs three things true at once: a fee that floats with congestion, a use that thins enough to weaken the network effect, and a pegged liability that holders can redeem at par at the moment both turn against them. The currency chain removes two of them, the first and the third. It runs on dedicated blockspace with a scheduled, predictable fee, one of the two designs the paper itself names as able to decouple cost from congestion, the other is a trusted Layer 2 whose trust is assumed rather than earned, since every Layer 2 in production runs on a single operator. The impediment the paper leaves unexamined is that operator, and the currency chain answers it: governed openly by those proper to it, audited, regulated, supervised, elected. The third condition it removes by structure, and that is what gives the certainty. Every unit the currency chain issues is a claim on the fiat in its reserve pool, and it can issue no more than the pool holds. Full reserve makes par a structural fact rather than a promise: there can never be more claims than money behind them, and no peg is left to break in a rush. The central-bank rail the ECB and the BIS reach for is a different answer to a different part of the problem, and our chain is no rival to it: a currency chain can settle its cash leg on the central bank's own money. The remedy here is the governed currency chain, not the resource beneath it.

Groot itself, the permissionless layer the result is actually aimed at, removes that same third condition by a different route: it has no peg to run from at all. The Gaju is a mined coin, not a redeemable claim, so the central ingredient of the run is simply absent. What remains is congestion, and the one place it could bite is Groot's own work, which is to be the high seas between jurisdictions, the neutral water over which value moves from one nation's base chains to another's. That bites only if its capacity is misread, and the capacity is real. The base layer carries more than three hundred transactions a second, already past the peak of the Tokyo Metro's contactless system, among the busiest payment networks on earth, and it expands far beyond that through state channels. A state channel is a direct off-chain link structured between two parties, touching Groot only when it opens and when it closes. Each channel handles more than five hundred transactions a second, and the number of channels is bounded only by the hardware put to it: a single MacBook M4 Pro sustains more than a thousand of them, so one ordinary machine clears on the order of half a million transactions a second, and the figure scales linearly with the machines added. Where value crosses between two or more Associate Chains, a channel structured between them carries the traffic off the base layer while only its opening and its closing touch Groot, and a regulated entity that sits on those chains can, with the authority of each, carry that same interchange on its own trusted rail. Under sustained load the fee on Groot's base layer can rise, and it is meant to: the pressure pushes that interchange onto the chains and channels built to carry it, and leaves the base layer for bulk settlement between chains and the exit of last resort.

Settlement runs as a single atomic transaction: both legs move together or neither moves, so there is no instant at which one party has delivered and the other has not. Within a single currency this asks nothing of Groot. An asset tokenised on a securities chain settling against money on a currency chain under the same national hierarchy settles inside that hierarchy, both legs in one movement, the gap between delivery and payment closed without any crossing of jurisdictions. Groot earns its place only where the settlement crosses currencies, and that is where the oldest and most expensive risk in settlement lives. Herstatt risk takes its name from the German bank that failed in the middle of a foreign-exchange settlement in 1974, after its counterparties had paid it but before it had paid them. Across currencies, two currency chains settle payment against payment through the Gaju, the neutral asset held only for the instant of the swap, and because the transaction is atomic there is no such window: it completes in full or it does not happen at all. A European investor buying United States equities settles the dollar equity against the dollar chain inside the United States hierarchy and the euro-to-dollar leg through the Gaju, the whole closing in one atomic settlement, in seconds, with no central counterparty and no chain of correspondents. The central counterparty that exists to net exposures and guarantee settlement becomes unnecessary rather than merely faster, and the cycle collapses from a day or two to seconds, releasing the collateral and the capital that the settlement window ties up across an institution's whole book. The edges of the claim are exact: it removes counterparty risk in the atomic, on-chain case; it does not, on its own, replace credit intermediation, the provision of foreign-exchange liquidity, or the netting of exposures that live off-chain. A central counterparty does real work, and that work does not vanish; for the one thing atomic settlement is built to do, it does it without the counterparty.

The Gaju that does this work is a mined coin, not a token. Its supply is fixed at one trillion, issued over an eighty-seven-and-a-half-year Fibonacci curve, with no issuer and no foundation behind it, on the same footing under Swiss law as Bitcoin, at a mining cost of somewhere between a tenth and a half of one United States cent. It is a claim on no one, and that is the property that lets it serve as neutral settlement between parties who would never accept a claim on each other.

The model is a complement to central bank money, not a replacement for it. Groot supplies the common anchor for convertibility across chains that the ECB says is missing and the BIS says does not exist across jurisdictions. Central bank money stays the ultimate settlement asset within each chain. The neutral layer reaches only the cases that coordination between jurisdictions cannot, which is exactly where the BIS itself concedes there is no universal settlement asset. We are not proposing to replace the two-tier system, but to supply the ground beneath it, for the cases the system's own architects admit it cannot reach.

A bundled issuer like Circle cannot simply take up this model, and a governed coordinator like Canton cannot simply turn itself into neutral ground, for reasons that are architectural rather than a matter of competence or intent. To unbundle the reserve yield from the coin is to dissolve the business that captures it. To make a synchroniser neutral is to remove the governing cohort that runs it, which is to stop being a synchroniser at all. They could re-architect, but the act of doing so dissolves the present structure rather than extending it. Where the standards work is good, it should be said so, and the Monetary Authority of Singapore's Global Layer 1 is good. The precedent for placing core infrastructure into a neutral, member-owned vehicle is long established. BankAmericard was placed in a member cooperative in 1970 and renamed Visa in 1976, a business whose net revenue reached around forty billion dollars in its 2025 financial year; the Chicago Mercantile Exchange's Class B structure gave its members six of nineteen directorships on roughly ten per cent of the equity; the London Metal Exchange was bought by Hong Kong Exchanges in 2012 for one point three nine billion pounds, a sale its shareholders approved by more than ninety-nine per cent. Neutral, member-owned infrastructure is not a novelty: it is how the most durable rails in finance were built, and GajuLayer1 AG is the single technical partner that builds it here.

The BIS, and the choice it now faces

The chapter of the twenty-third of June does not only diagnose; it prescribes, and the prescription is close to what we have already offered. The BIS calls for tokenisation of currencies to be brought inside the regulated two-tier system through a unified ledger, "implemented as a system of interoperable networks," holding together tokenised central bank reserves, tokenised commercial bank money, supervised private monies and tokenised assets, all anchored in central bank money, with clear functional separation, atomic settlement, and interoperability in the place where the walled gardens used to be. It points to Project Agorá, eight central banks and more than forty private institutions, as its flagship demonstration that cross-currency settlement can be made atomic while each jurisdiction keeps domestic control of its own reserves. The central bankers' central bank has, in other words, confirmed both halves of the case this essay has made: the diagnosis, that stablecoins fall short of money and fragment across chains, and the prescription, that the answer is a two-tier system anchored in central bank money, with functional separation and atomic settlement.

Project Agorá is a coordinated, governed construct; it works because eight central banks agreed to it and submitted to a shared arrangement. That agreement is there to be had inside a club of aligned jurisdictions. It is not there to be had across rival ones, and the BIS says as much itself when it concedes that across jurisdictions there is no universal settlement asset and that singleness holds only within each currency. Where jurisdictions will not submit to a common operator, and between rivals they will not, there has to be neutral ground, or there is no cross-jurisdiction singleness at all. Groot is that ground. The Gaju is that asset. I claim no endorsement from the BIS, and there is none; the claim is narrower than endorsement, and stronger. Our architecture realises the principles the BIS has set out, and supplies the neutral cross-jurisdiction layer that the BIS otherwise leaves, by default, to foreign exchange and correspondent banking, because its own model has nowhere else to put it.

The institution has, in its own measured language, said a great deal of what we have said: that the chains dressing themselves up as decentralised are nothing of the sort, that a permissioned network with a governing cohort is a walled garden, that a private claim on a congested public rail is not money and cannot hold par when stress arrives. Anonymous proof-of-stake manufactures the look of trust without the substance of accountability: the landlord who takes the rent every month and will not come to fix the plumbing when it bursts. An institution that wants par, finality, functional separation and atomic settlement, and that understands why walled gardens fail, would on reflection see the sense in a neutral layer it does not have to operate and cannot be accused of capturing. On that reading, the BIS and the work described here want the same world, and the only thing left to settle is who builds the ground floor.

The other reading is that the call for a unified ledger anchored in central bank reserves and run within permissioned rails is not really about singleness at all, but about control: a consolidation of authority over the rails of money, dressed as prudence, in the manner of the European Union's long habit of meeting every problem with another tier of central administration. On that reading, the neutral layer is the one thing the institution cannot welcome, because neutral ground is the single place its writ does not run, and an exit that disciplines the system is intolerable to anyone whose interest is in the system's monopoly rather than in its soundness.